Summary: In prior posts, I set-up the following issue …

Some policy analysts (typically left-leaning) such as Robert Reich, Bill Clinton’s former Secretary of Labor argue that “Most Americans pay more in payroll taxes than in income taxes … payroll taxes take a much bigger portion of the paychecks of lower-income Americans than of higher-income … Viewed as a whole, the current tax system is quite regressive.”

http://economistsview.typepad.com/economistsview/2007/10/robert-reichs-p.html

Other analysts such as the Urban Institute clarify “The payroll tax is very regressive with respect to current income: The average tax rate falls as income rises … (But) the regressivity of the payroll tax is mitigated to a substantial extent when Social Security and Medicare benefits are considered as well.

http://www.urban.org/publications/1001065.html

But analysts generally “punt” the question “what is the effect when both payroll taxes and their benefits are considered ? ” Why ? In part, I suspect, because they know the answer doesn’t fit their politics … and, in part, because the analysis is challenging — with many nuances and moving parts.

In this post, I take a shot at the “combined effect” question by applying some fundamental financial analysis tools.

Specifically, I treat Social Security benefits as an annuity stream to individual retiring workers and I treat annual payroll taxes over a worker’s career as periodic “premiums” that get applied to the “purchase” of the annuity.”contract”. After adjusting for inflation, the difference between the present value of the expected benefits stream and the present value of the “premiums” paid over the years is, in essence, the real tax that a plan participant pays.

The answer: low wage earners pay practically nothing for their benefits — their contributions are simply a forced saving for their retirement benefits. High earners get relatively little of their contributions back — in effect, paying a tax rate over 60%

* * * * *

Analytical Details

Regarding Social Security, a Congressional Joint Economic Committee reports:

“The rapid growth in payroll taxes over the past 40 years has imposed a large burden on working Americans. This burden has fallen disproportionately on low-income workers.

However, in the context of a comprehensive tax policy, it is misleading to focus on the short-term burden imposed by payroll taxes without accounting for the future benefits they provide through the Social Security program.

Social Security benefits are paid according to a progressive formula that gives low-wage workers a better rate of return on their contributions than it gives high-wage workers. The progressivity of the benefit formula outweighs the disproportionate burden imposed by the tax.

As a result, low-wage workers can expect to receive benefits that exceed the sum of their and their employers’ payroll tax contributions. Middle- and high-wage workers, on the other hand, can expect to pay substantially more into the system than they will receive in benefits.

Overall, middle- and high-wage workers subsidize the income and payroll tax liabilities of low-wage workers, leaving most low-wage workers with net negative tax liabilities throughout their lifetimes.”

http://www.house.gov/jec/fiscal/tx-grwth/payroll/payroll.htm

* * * * *

Here’s what the Joint Economic Committee is talking about:

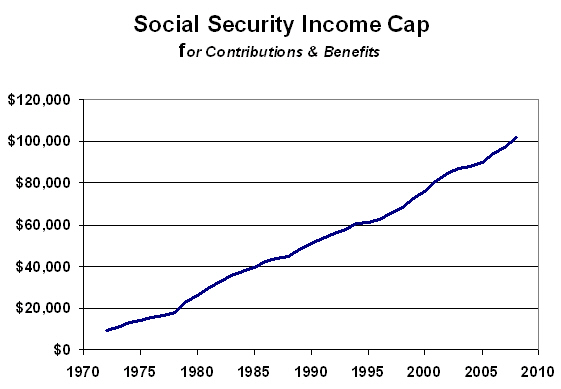

The amount employees have deducted from their paychecks is determined by the Social Security tax rate and annual income “caps” – the maximum amount of wages subject to the tax. The Social Security tax rate has been flat for almost 20 years; and the income cap has consistently increased over the years.

Currently. an employee’s Social Security tax rate is 6.2% on annual wages up to $102,000. For high earners, the rate drops to zero for any wages over $102,000 in a given year.

For example, somebody earning $50,000 has $3,100 deducted from their paychecks [6.2% times $50,000]. Somebody earning $102,000 has $6,324 deducted [the same 6.2% times $102,000]. Somebody earning $200,000 has $6,324 deducted [6.2% times the $102,000 income “cap”; 0% on wages over $102,000] — so their effective rate drops to 3.2%. The more somebody earns over the $102,000 income cap, the lower their effective rate.. By definition, that’s a regressive tax, right?

* * * * *

Not so fast. There’s more to the story.

First, the 6.2% tax rate is literally only half of the story. Employer’s are legally obligated to pay a matching amount to the Social Security fund (similar to a company matching 401-K contributions — but certainly not voluntary). So, the applicable rate is really 12.4% (2 times 6.2%) — up to $102,000 in earnings.

-

Note: Most economists argue that, in the final analysis, employees bears the full burden of the employer’s matching amounts since employers probably cover the tax by reducing wages – or viewed conversely, employers would raise wages if they weren’t stuck paying the Social Security taxes. That conclusion is debatable, but we’ll accept it and treat the full.12.4% as a charge incurred by the employee).

-

Note: Employers can deduct their share of the contribution for income tax purposes, but workers’ shares are not tax deductible. For simplicity, we’ll ignore that taxing distinction.

Obviously, doubling the rate ups the ante, but it doesn’t make this payroll tax any more (or less) regressive or progressive.

Second, while Social Security payroll deductions fit the technical definition of a tax — i.e. a “levy” imposed on an individual or a legal entity by a government — they don’t act like most taxes.

Most taxes are collected to fund a common interest (say, defending the country or building a bridge). The amount that a taxpayer gets charged, is de-coupled from the benefits they (the tax payers) may receive. That is, the taxpayer may or may not actually receive a direct (or indirect) benefit, and any benefits that they do receive are almost always non-monetary (e.g. riding on a freshly paved highway, calling for an EMT crew)..

Social Security is different – it is both monetary and coupled. With Social Security, the benefits are strictly monetary – monthly retirement income checks – and are based on a formula that is explicitly coupled to the beneficiary’s career income and corresponding contributions to the Social Security fund.

* * * * *

Let’s illustrate Social Security math using a hypothetical retiree. We’ll call him Harry the High-earner — for shorthand referencing, just plain old Harry.

Assume that Harry – an unmarried guy — turns 66 on January 1, 2008 and decides to retire — claiming his full Social Security benefits.

-

Note: if Harry had retired at an earlier age, say 62, he would have started receiving scaled down benefits a few years earlier.

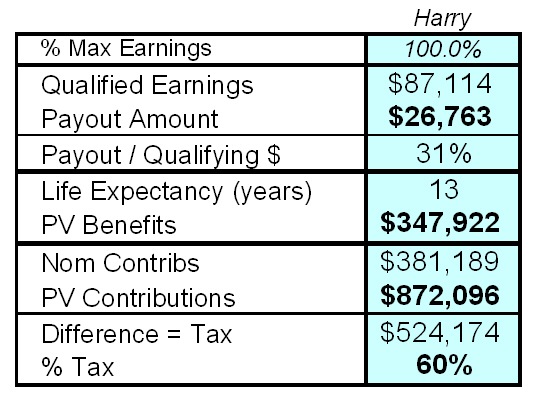

Also assume that Harry has been working since age 25, that he earned precisely the maximum taxable base earnings each year (i.e. the year-by-year equivalent of 2008’s $102,000 wage cap), and that he and his employer both paid the applicable Social Security rates each year on those earnings.

Applying historical Social Security rates and income caps, during the 41 year period (since age 25), Harry would have had $190,595 deducted from his paychecks. His employer would have matched that amount dollar-for-dollar.

Again, economists usually argue that employee’s bear the burden of their employer’s contributions since they are simply a diversion of higher wages that might have been paid to the employee. So, Harry’s total contributions – including his employers’ portions — are $381,189.

The $381,189 is a “nominal” amount since it doesn’t reflect the impact of inflation over the years. Using government-provided inflation indexing factors, the $381,189 has a “real” worth — in 2008 dollars – equal to $872,096. That’s how much Harry and his employer paid into the Social Security fund, adjusted for inflation.

http://www.ssa.gov/pubs/10070.html#a

Conceptually, when he retires and starts drawing benefits, Harry is taking the $872,096 in accumulated contributions (stated in 2008 dollars) and investing the whole amount in an annuity — a steam of checks that he’ll be receiving from the government.

How much is the annuity worth to Harry? That is, what’s Harry getting for his $872,096 ?

The annuity valuation has two main components: the amount of the periodic payments and the duration of the payment stream.

Social Security benefits are based on a relatively complex formula that factors historical earnings against a sharply dropping scale of payouts.

Specifically, the Social Security formula “looks back” over an employee’s career, picking the 35 years in which the employee earned the highest taxable wages (up to each year’s income cap). The employee’s top 35 years of taxed earnings are then indexed to reflect inflation – i.e. “inflated” to current day dollars — and then averaged. .

Then, the qualified earnings (i.e. the 35 year average) are plugged into the sliding scale formula to determine the initial annual amount to be received in Social Security benefits. 90% of the first $8,532 counts; 32% of the next $42,924 (up to $51,456) counts; and only 15% of any excess over $51,456 counts.

Since we’re assuming that Harry earned the maximum taxable income in each year, his top 35 years are the last 35 years (since the income cap has been consistently going up). His inflation adjusted average income over that period is $87,114.

Plugging the $87,114 into the Social Security benefits formula, Harry’s initial annual Social Security benefit will be $26,763 — 31% of his inflation adjusted average annual wages for his highest 35 years’ earnings.

How long will Harry be getting the payments?

That’s conceptually easy to answer: Until he dies.

-

Note: If Harry had been married, payments would come until both Harry and his wife die — since she would have survivor rights to his benefits).

Currently, the average life expectancy in the U.S. is 78 years. For simplicity assume that Harry is actuarially average, so he will get the $26,763 in annual benefits for 13 years — until age 78.

Harry’s total “annuity benefits” are $347,922 — 13 years times $26,763. Assuming that the $26,763 gets inflation adjusted in future years (i.e. the Social Security Administration boosts the benefit each year to relect inflation), then the $347,922 is — by definition — expressed in real 2008 dollars.

Pulling the parts together: stated in 2008 dollars, Harry (and his employer) paid $872,096 to get annuity benefits worth $347,922.

The $524,174 difference is the real Social Security tax that Harry paid — a whopping 60%

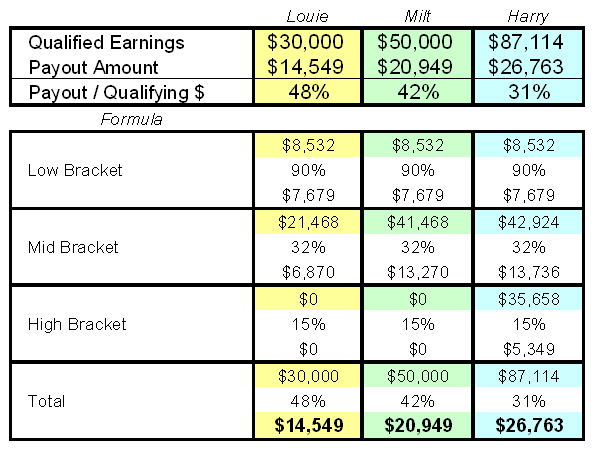

For comparison, let’s apply the same analytical logic and run the numbers for two other retirees who have exactly the same profiles as Harry (the high-earner), except that they earned less during their best 35 years.

Low-earning Louie earned an inflation adjusted average of $30,000 and mid-earning Milt earned an inflation adjusted average of $50,000. So, their respective calculated initial annual benefits are $14,549 (which works out to be 48% of $30,000) and $20,949 (42% of $50,000). High-earning Harry only got 31% of his inflation adjusted average wages in annual benefits.

For analytical simplicity, let’s assume that Louie and Milt earned a constant percentage of the Social Security income cap each year. Applying that assumption, their $30,000 and $50,000 wage bases translate to 34% and 57% of each year’s income cap. (Trust me and Excel Solver on the percentages).

Let’s assume that Louie and Milt – like Harry — have been working and contributing to Social Security since age 25. Then, we can multiply Louie and Milt’s income cap percentages (34%, and 57%) times each year’s income cap (keeping in mind that it has increased in most years) — multiply that number (annual taxable wages) times the Social Security tax rate in each year (the total of the employees’ and employers’ contributions) – and then sum across the years (from age 25 to age 65).

The answer: Louie and Milt kicked in a total of $131,272 and $218,276, respectively. Again, those are “nominal” totals, unadjusted for inflations.

Applying the Social Security Administration’s inflation factors – the same ones used for the benefits calculation — the nominal totals “inflate” to $300,328 and $500,547 in 2008 dollars.

The rest of the analysis is simply arithmetic: Louie kicked in $300,328 to secure an annuity with a present value (at retirement) of $189,131. The difference ($111,197) is, in essence, the implicit net Social Security tax that Louie paid — 37% of his inflation adjusted contributions.

Milt put in $500,547 to get $272,331 in benefits – an implicit tax of $228,215 – 46% of Milt’s inflation adjusted contributions. And trust me, below Louie’s qualifying income level, the rate drops further — very quickly.

* * * * *

The Bottom Line:

Social Security “payroll taxes” are fundamentally different from other types of taxes because they represent a future payment back to the contributor.

Thus. payroll taxes cannot be viewed in isolation, but must instead be viewed in the lifetime context of tax payments and retirement benefits. http://www.house.gov/jec/fiscal/tx-grwth/payroll/payroll.htm

When both the taxes on current wages and the eventual benefits realized are both considered, real tax rates increase with income and Social Security is then – by definition – a very progressive plan.

Case closed !

* * * * *

Want more from the Homa Files?

Click link => The Homa Files Blog

* * * * *

Leave a comment